The EU’s next Multiannual Financial Framework (MFF) will be negotiated under intense pressure: a tight budget, expanding demands for spending and growing disagreement over the Union’s priorities. This guide explains how the MFF works, clarifies the mechanics of EU budget negotiations, and identifies five key battles that will shape the outcome – budget size, policy priorities, structure and governance, conditionality, and revenue. The stakes are high. These negotiations will reveal whether the EU can agree on a budget that aligns with its ambitions for a free, secure and competitive Europe – or whether it will once again become mired in familiar disputes over net balances and sectoral red lines.

1. The MFF circus is back in town

The next MFF will hardwire political choices well into the 2030s. As the EU’s seven-year budget, it determines the overall volume of EU spending, decides which priorities receive funding, and defines how much flexibility is available when the unexpected occurs. It arrives at a moment when expectations of the EU are rising, while fiscal room for manoeuvre in many Member States is shrinking. Calls to support Ukraine, strengthen security and defence readiness, navigate geo-economic tensions, boost competitiveness and industrial capacity, and accelerate the green and digital transitions all expose the limits of a rigid budget. They also underscore what is at stake in the months ahead.

Against this backdrop, the European Commission published an ambitious proposal for the next MFF in summer 2025. It represents a more far-reaching overhaul than in any previous cycle. Alongside a larger budget – 1.26% of gross national income (GNI) (including 0.11% for NGEU repayments), compared with 1.07% in the current MFF – the Commission proposes a radical simplification of the budget’s structure to enable funds to be used more efficiently and deployed more flexibly as new challenges arise. To spend more strategically, it also suggests shifting relative priority away from traditional areas such as the Common Agricultural Policy and cohesion towards competitiveness and defence.

The Commission’s proposal is a huge step in the right direction – but it is far from settled. The proposed architecture has survived early Council discussions and strong pushback in the European Parliament, yet the most difficult bargaining begins once the figures are firmly on the table. At the same time, key questions concerning governance and implementation remain unresolved.

This guide walks you through the essentials of the MFF and offers a roadmap to the negotiations ahead. It begins with the fundamentals of the EU budget – its size and functions, the different spending ceilings, management types and the revenue side. It then turns to the negotiations, explaining the rules of the game, the main actors and the expected timeline. Finally, we identify five battlegrounds that will shape the next MFF: the overall size of the budget; which priorities gain or lose; the struggle over structure and governance; the reach of rule-of-law and human rights conditionality; and, ultimately, who pays.

2. Back to basics: how the EU budget works

This section revisits the main features of the EU budget. If you live and breathe the MFF and organise your household finances in terms of commitments and payments, this may not be for you. But because this exercise comes around only every seven years, it is worth reminding everyone else that the EU budget differs from national budgets in several important respects.

2.1 The EU budget is small – and that matters for what we can expect from it

The EU budget is tiny compared with national budgets. In 2024, total expenditure, including debt-financed spending from NextGenerationEU (NGEU), stood at €247 billion, or 1.38% of EU GDP. Without NGEU borrowing, it would have amounted to €174 billion, or 0.97% of EU GDP. These figures fluctuate over the MFF cycle, but the overall order of magnitude remains broadly the same. For comparison, the German federal budget in 2024 amounted to €477 billion, or roughly 11.03% of German GDP – around ten times the size of the EU budget. Total public expenditure in Germany stood at €2,082 billion, or 48.36% of GDP – more than 40 times the size of the EU budget.

The implication is clear: EU spending cannot be the sole, or even the predominant, source of public funding in any major policy area. There is only one significant exception in which public funding is fully Europeanised – direct payments to farmers. That is why they account for such a large share of the budget: in 2024, around 23% of expenditure excluding NGEU spending. Unless Member States are willing either to increase the overall size of the budget dramatically or to narrow its scope substantially, the EU budget will remain complementary to national spending.

We therefore need to be clear about what the EU budget can do – and what it cannot. It is unrealistic to expect EU funding alone to meet the financing needs of major policy objectives. The EU budget will not, by itself, resolve shortfalls in defence spending, infrastructure investment, or higher education and research funding. It can, however, make a difference in three important ways:

- Redistribution. The EU budget can act as a financial transfer mechanism between Member States, enabling poorer countries – and increasingly those with more limited fiscal space – to invest more in common EU objectives. This is the core rationale of cohesion policy and explains why, in some less affluent countries, EU spending represents a substantial share of public investment. In Bulgaria, for instance, EU cohesion funds amount to roughly 56% of public investment across the MFF cycle.

- Nudging. The EU budget can encourage Member States to align with EU policy objectives by co-financing national spending, subject to certain conditions – such as implementing reforms or complying with EU standards. This approach works best where countries stand to gain more than they contribute, as is the case for net beneficiaries of the EU budget. It has limits for net contributors: from their perspective, retaining funds domestically may appear more attractive than transferring them to Brussels and receiving them back with a checklist attached.

- Spending better together. The EU budget enables the Union to invest collectively in areas where joint action clearly outperforms national efforts. EU research and innovation funding, as well as many external instruments such as pre-accession assistance, are good examples. Joint spending allows the EU to pool resources, avoid duplication and achieve economies of scale.

For any new EU spending proposal, two basic questions should therefore be asked: first, does it reflect a realistic expectation given the size of the budget; and second, which of these three functions does it seek to serve?

2.2 Two types of budgets, numbers, and ceilings – and what they mean

Unlike national budget planning, EU financial planning does not rely solely on annual budgets but is anchored in the multiannual framework (MFF). Key decisions on the overall size of the budget, spending ceilings for broad policy areas (“headings”) and programmes, as well as revenues, are fixed in the MFF for a period of typically seven years rather than a single year. The annual budget then specifies the actual spending and revenue for that year within the limits set by the MFF. The MFF negotiations are therefore one of the few moments when the EU’s strategic priorities and their funding can genuinely be debated. Annual budget talks – at least for now – play second fiddle.

Both the MFF and the annual budgets contain separate ceilings for commitments (what the EU can legally promise) and payments (what the EU can actually spend), and the two can differ substantially. For many EU programmes, funds are committed in one year but paid out in another – sometimes even under a subsequent MFF. In Brussels terminology, these outstanding commitments are referred to as reste à liquider (RAL). As a result, actual annual spending – meaning the payment appropriations required each year – is driven largely by commitments made in earlier years and can no longer be altered. The exact amounts due in future years are often difficult to predict because, apart from direct payments to farmers, most EU spending is tied to long-term investment projects that are not easily adjusted.

Beyond the commitment and payment ceilings in the MFF, the Own Resources Decision (ORD) sets overall ceilings for annual commitments (currently 1.46% of GNI) and payments (currently 1.40%). The MFF ceilings cannot exceed these limits. The gap between the MFF ceilings and the ORD ceilings – known as “headroom” – can be used as a legal guarantee for debt repayment. In 2020, for instance, the EU temporarily raised the ORD payment ceiling from 1.40% to 2.00% of GNI to create additional headroom and support NGEU borrowing. Some EU programmes are financed over and above the ceilings – meaning beyond the MFF but within the ORD limits. This currently applies, for example, to support for Ukraine and the Flexibility Instrument. The European Peace Facility, by contrast, sits entirely outside the MFF and is independent of both MFF and ORD ceilings.

2.3 Who actually spends the money: direct, shared and indirect management

Alongside debates about political priorities, the question of who actually spends EU money is central to the design of the MFF. The EU uses three main management modes. Under direct management, the Commission or an EU executive agency awards grants, procurement contracts or prizes itself and pays beneficiaries directly. This is typical for research and innovation programmes. Under shared management, the Commission sets the general rules, but the money effectively flows through Member States. This is the default model for cohesion policy and much of agricultural spending. Under indirect management, the Commission entrusts implementation to third parties – such as the European Investment Bank or international organisations – often in order to draw on specialised expertise or financial instruments.

These categories are not merely technical; they are politically sensitive. Many Member States prefer shared management because it keeps the steering wheel firmly in national and regional hands. Shared management programmes provide pre-allocated funding streams, allow governments to align EU funding with domestic priorities, and enable them to demonstrate visible ownership at home. The downside is that it leaves the EU with less direct control when trying to steer spending towards common objectives.

2.4 The weird way the EU budget is funded

Another crucial difference from national budgets is that the EU budget is expenditure-driven rather than revenue-driven. National budgets depend on the expected revenue and the level of debt a government is willing to issue. The EU budget works in the opposite direction. When the Council and the European Parliament adopt the annual EU budget, they are constrained not by projected revenue for the coming year but by the commitment and payment ceilings laid down in the MFF. As long as payment appropriations remain within those ceilings, Member States are legally obliged to foot the bill.

That bill is covered by different revenue streams. Similar to national tax income, the EU has fluctuating own resources: customs duties (known as traditional own resources), a fixed call rate on national VAT bases, and a contribution linked to non-recycled plastic packaging waste. These are supplemented by other revenues, including administrative and financial income, default interest, fines and surpluses carried over from previous years. The key feature, however, is that any remaining gap between these revenues and the expenditure level set in the annual budget is automatically filled by national contributions based on gross national income – the GNI-based own resource. It is as if, at the national level, the income tax rate is automatically adjusted each year to match spending needs. The GNI-based resource provides by far the largest share of EU funding, exceeding all other resources combined (excluding NGEU borrowing).

Crucially, none of these revenues is collected directly by the EU itself. For most own resources, the EU simply receives payments from national budgets. Thus, except for custom duties – which countries hand over after skimming a 25% collection fee, own resources are largely formulas for allocating a pre-determined financing burden among Member States. In that sense, the rebates granted to some of the largest net payers are no different. They simply adjust how that burden is distributed relative to the baseline GNI key.

This has an important implication. Unlike at national level, introducing new revenue streams does not automatically increase the size of the budget. Additional revenues would simply reduce the GNI-based contributions required from Member States and redistribute the financial burden. The overall level of expenditure is capped by the ceilings set in the MFF – not by the volume of revenue available.

3. MFF negotiation 101: the rules of the game

In July 2025, the Commission kicked off a two-and-a-half-year negotiation in which the EU’s entire financial architecture is at stake. This section sets out the rules of the game: what is being negotiated, who holds the decisive votes and how this cycle is likely to unfold.

3.1 What we mean by “MFF negotiations”

When we talk about the MFF negotiations, we usually mean much more than just the MFF Regulation. In July and September 2025, the Commission proposed a package of legal texts with three main components:

- The MFF Regulation sets the annual ceilings for commitments (what the EU can legally promise) and payments (what it can actually spend) over the seven-year period. For commitments, it also determines how spending is divided across broad policy areas – known in EU jargon as “headings”, “pillars” or “categories”. The current MFF has seven headings; the Commission’s proposal for the next one reduces this to four. The MFF Regulation requires unanimity in the Council and the consent of the European Parliament.

- The Own Resources Decision (ORD) governs how the budget is financed. It sets the maximum amounts the EU can commit and collect each year. At present, the ceilings stand at 1.46% of GNI for commitments and 1.40% for payments. The Commission has proposed raising them to 1.81% and 1.75% respectively. The ORD also defines the EU’s revenue sources. It requires unanimity in the Council and, in most Member States, ratification by national parliaments. Parliament is consulted but has no official say.

- A whole host of supporting or sectoral regulations set the rules for EU spending programmes. Some apply horizontally across multiple programmes – for example, the expenditure tracking and performance framework – while others govern specific policies such as the Common Agricultural Policy (CAP) or Horizon Europe. These are usually adopted under the ordinary legislative procedure, meaning they require a qualified majority in the Council and a majority in Parliament.

3.2 The main characters: why much depends on the Council

These three components are usually treated as a package and, at least on the Council side, negotiated together. Crucially, the way the talks are organised in this cycle already locks in the main novelty of the Commission proposal. The Danish presidency created four MFF working parties – one overarching group and one for each of substantive heading – effectively anchoring the new structure from the outset. For a handful of less controversial sectoral regulations, the Council can agree on partial negotiation mandates early on, allowing talks with Parliament to begin before the entire package is settled. This happened in December 2025 for the Connecting Europe Facility and the Single Market Programme. However, the unanimity required for the MFF Regulation and ORD gives Member States a powerful lever. Governments can link progress on these files to other contentious issues and, in doing so, they can pull elements of sectoral legislation into the realm of unanimity-based bargaining. Ultimately, Council negotiations usually culminate in lengthy European Council conclusions. These fix the headline numbers for the MFF Regulation, outline key decisions on revenue and contain a long list of rules later implemented in sectoral legislation.

In practice, this process revolves around the so-called Negotiating Box, affectionately dubbed Nego Box. This is essentially a fancy name for draft European Council conclusions. Early versions contain many square brackets, marking unresolved issues. With each revision, the aim is to reduce those brackets as compromises are found. During the first year and a half or so, the boxes are prepared by successive Council Presidencies, each typically drafting one or two versions. The Danish presidency published an initial Negotiating Box on the MFF’s structure in December 2025, without financial figures. As negotiations intensify, updates become more and more frequent. In the final stretch – shortly before a box gets adopted as formal European Council conclusions – responsibility typically shifts to the President of the European Council. Preparing the boxes entails an important power of the pen: Whoever drafts the box decides which issues are included, in what level of detail, and, which elements of sectoral legislation are pulled into the text – thereby making them subject to unanimity. That is what makes the Nego Box the central steering instrument of the negotiations.

The package structure of the MFF also places the European Parliament at a structural disadvantage. Because both the MFF Regulation and the ORD require unanimity in the Council, the Council presidency seeking Parliament’s consent for the MFF Regulation has limited room to depart from the agreed European Council conclusions. Time and again, Parliament has entered negotiations with ambitious demands, only to secure relatively modest concessions in the final stages. The reason is simple: it is reluctant to trigger a last-minute reopening of the deal in the Council. For a brief moment in November 2025, this pattern seemed different. Deeply opposed to the proposed changes in funding for cohesion and agriculture, Parliament threatened to reject the draft MFF Regulation as a starting point for negotiations. However, after Commission President Ursula von der Leyen proposed amendments to the Commission’s text – including stronger language on regional involvement and limited concessions for rural areas – Parliament withdrew its threat.

The Commission’s role in all this is worth noting. Both during the November 2025 clash with Parliament and in the January 2026 negotiations on the Mercosur trade agreement, the Commission suggested amendments to its own proposal to help broker compromises. Formally, the Commission has no decision-making role in the MFF negotiations once it has tabled its proposal, so these amendments are technically not binding. In practice, however, both the Council and Parliament have so far treated them as legitimate negotiation material.

3.3 Tight timing: durations and deadlines

The current MFF expires at the end of 2027, as do most spending programmes. Legally, the EU could continue making payments and honour outstanding commitments under the final-year ceilings of the existing framework. But without a new MFF, it cannot properly plan or launch new programmes. That would create uncertainty for beneficiaries and increase the risk of funding gaps. The ORD, by contrast, has no expiration date. Until a new one is adopted, Member States remain obliged to contribute under the ORD currently in force.

The choreography of reaching European Council conclusions typically follows a familiar script. First comes a summit at which Member States fail to agree – something almost everyone expects – but clarify the final sticking points. A second summit, held a few months later, then actually lands the deal.

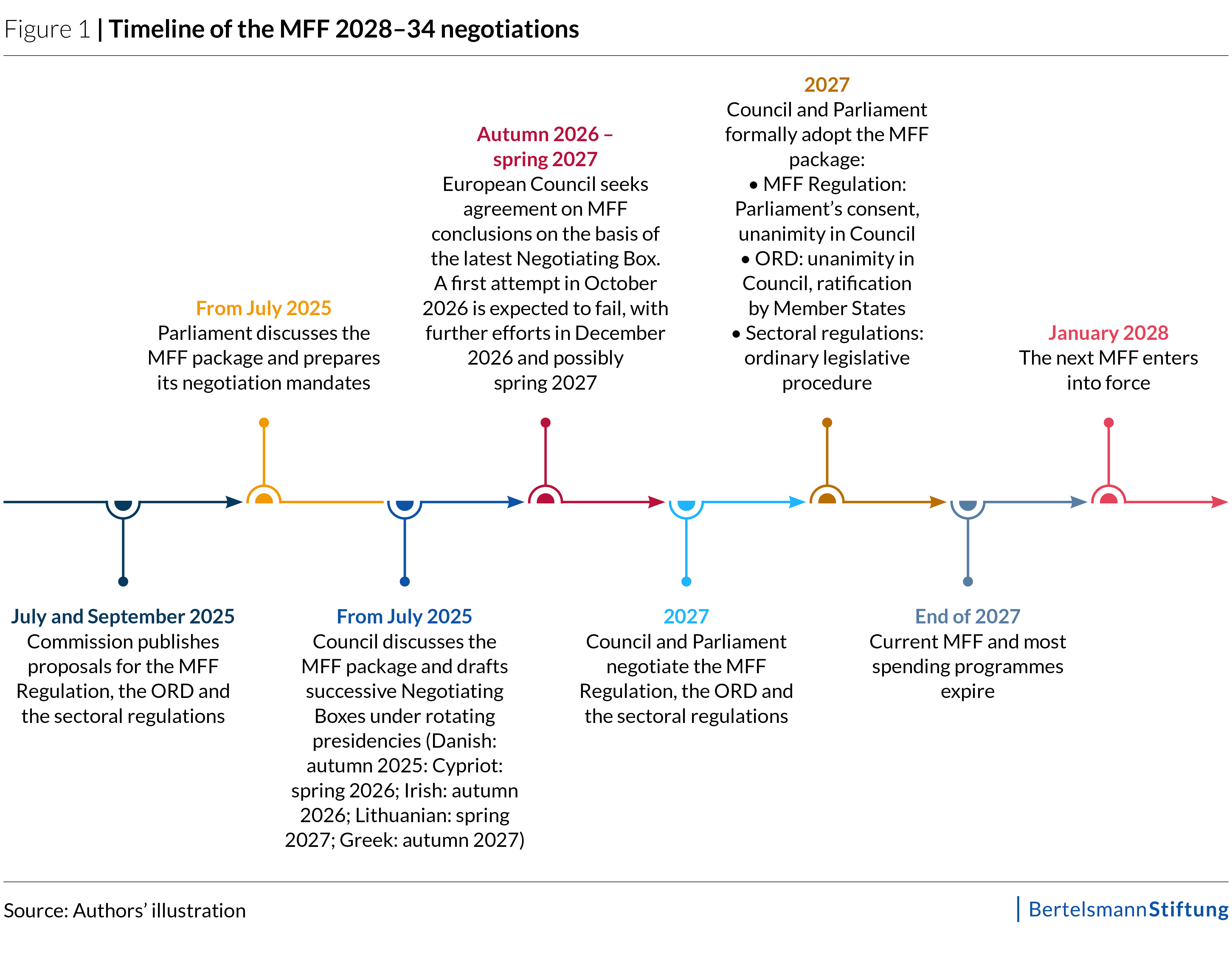

This time, the Council has set itself an ambitious timetable (Figure 1). It aims to reach agreement on the MFF package by the end of 2026 – one year before the current framework expires and roughly six months earlier than in the previous cycle. The Danish presidency in autumn 2025 focused on structure and governance. The Cypriot Presidency, which took over in January 2026, opened negotiations on the financial figures. The Cypriot and subsequent Irish presidencies occupy the awkward middle phase of the process, when the lack of sharp deadline pressure tends to slow progress. That pressure increases markedly in the final year of the current MFF – under the Lithuanian and Greek presidencies – when Member States face the prospect of programmes simply running out. The European Council is therefore expected to attempt agreement at its October 2026 summit, likely without success, and again in December 2026, with improved prospects. Even so, a final deal may only emerge in spring or summer 2027, after the planned French presidential elections.

The earlier the Council strikes a deal, the better. Once political consensus is in place, the Council and Parliament still need time to negotiate the file and formally adopt the package. Parliament must give its consent to the MFF Regulation, and the Council must unanimously approve both the MFF regulation and the ORD.

4. Five battlegrounds that will decide the MFF

Everyone (mostly) agrees on the shopping list. The real dispute begins when the bill arrives: who pays, how much, who controls the money – and what gives when fiscal reality bites. Five battlegrounds will shape the outcome of the next MFF.

4.1 Size: How big is the pie?

There is no shortage of demands for EU spending. Calls to strengthen Europe’s competitiveness, resilience and decarbonisation – as urged by Mario Draghi – and to scale up European defence production point to a vast public investment gap. At the same time, long-standing priorities do not simply disappear. Farmers and governments in less affluent Member States continue to expect robust EU support for agriculture and cohesion.

NGEU further complicates the debate about size. Late in the previous MFF negotiations, the Covid-19 pandemic triggered the creation of NextGenerationEU (NGEU). It added €390 billion in grants – roughly 0.4% of EU GDP – to the EU’s financial firepower. Formally, these funds sit outside the MFF ceilings and the annual EU budget, but they are very much part of the EU’s broader funding landscape. NGEU will also add an equivalent amount of debt to the EU’s balance sheet. The EU must pay interest on that debt and, under current law, begin repaying the principal in 2028. Any decision to reschedule or extend repayments beyond 2058 would require unanimity, as the repayment schedule is written into the Own Resources Decision. The Commission therefore proposes setting aside €24 billion per year (in current prices) for interest and capital repayments – €168 billion over 2028-2034. The consequences are clear: the end of NGEU spending will not only tear a hole into the EU’s purse, but debt service will also eat up a substantial chunk of the next MFF.

To respond to these spending pressures, the Commission has proposed a total of €1.98 trillion in commitments (current prices) for the next MFF. The headline figure of “€2 trillion” has triggered fierce resistance from so-called frugal countries. Yet two caveats are important. First, multiannual budgets are best assessed as a share of GNI rather than in absolute terms, as inflation distorts the picture. The proposed volume corresponds to 1.26% of GNI – just 0.14 percentage points above the 1.12% agreed in the previous cycle. Frugal capitals argue that this understates the increase: because the EU budget was adjusted using a fixed 2% deflator while actual inflation turned out much higher, the current MFF effectively shrank to around 1.02% of GNI in real terms. On that basis, the jump to 1.26% appears more substantial. However, this gap mainly reflects imperfect inflation adjustment rather than a change to the politically agreed volume, so it is a contested benchmark for negotiations. Second, NGEU debt repayment will absorb around 0.11% of GNI over the next MFF period. That means the amount available for new or ongoing programmes increases by only around 0.03 percentage points. From the perspective of frugal Member States, of course, the distinction matters little: whether the money funds new investment or services debt, they still have to finance it.

There is another constraint. Many Member States are neither willing nor able to contribute more for economic as well as political reasons. France illustrates the dilemma. While Paris often calls for an ambitious EU budget, it faces domestic consolidation pressures and limited fiscal space. At the same time, Eurosceptic voices in the National Assembly increasingly question the value of France’s EU contribution. As the 2027 presidential election approaches, domestic politics will weigh ever more heavily on France’s position. This time, therefore, resistance to a larger budget may come not only from the usual frugal suspects such as the Netherlands or Germany – but also from Member States that simply lack room to pay more.

In short, major cuts to the Commission’s proposed volume appear likely. And for the first time, debt servicing will enter the EU budget as a major line item. That leaves two options: the EU will have to scale back existing programmes, limit space for new priorities – or both.

4.2 Priorities: who gets what?

Joe Biden once recalled his father telling him: “Joey, don’t tell me what you value. Show me your budget; I’ll tell you what you value.” Applied to the EU budget, we could conclude that the EU overwhelmingly values farmers and regions. Today, about a third of the budget goes to the Common Agricultural Policy (CAP). Around a quarter of the total budget is devoted to direct payments to farmers. Because this is the only major policy area in which public support is fully Europeanised and not complemented by national spending, these payments inevitably appear oversized. Another third of the budget flows to European regions through structural funds under shared management, with allocation keys fixed at the beginning of each MFF. These funds pursue multiple objectives, from reducing regional disparities to fostering sustainable growth, but the first-order logic of distribution remains geographic. In practice, they function as an implicit transfer system between Member States. Taking away the roughly 10% for external action, only about a quarter of the budget remains for priorities pursued at the EU level under direct management – including research, innovation, decarbonisation and administrative expenditure.

Consistent with its diagnosis of rising investment needs in innovation, competitiveness and defence, the Commission has proposed a shift in emphasis. Under its draft, agriculture and cohesion together would account for 37% of total commitments – still the largest single chunk of the budget, but notably less than at present. Heading 2, covering competitiveness, infrastructure, culture and security, would rise to 30%. Heading 3, covering external action, would account for 11%.

As negotiations move forward, however, experience suggests that this balance usually tilts back towards CAP and cohesion. Member States often favour funds under shared management because they provide predictable national returns – as opposed to EU-wide programmes without geographic pre-allocations. In the past that has even been true for countries like Germany, which, under pressure from its regions, has pushed for a sizeable envelope for the shared management funds even though it typically gets much better financial returns from programmes such as Horizon Europe.

What is different this time, however, is that the Commission has proposed placing agricultural and cohesion funding into a single instrument: the National and Regional Partnership Plans (NRPPs). That changes the dynamic. Instead of a straightforward contest between shared management and centrally managed programmes, the tension may shift within the shared-management envelope itself. The Commission’s suggested amendments to its own proposal illustrate this. In response to criticism from Parliament in November 2025, Ursula von der Leyen proposed a 10% spending target for rural areas within the NRPPs. Then, in January 2026, in an effort to secure Italy’s support for the Mercosur trade agreement, the Commission suggested granting Member States early access to €45 billion from the NRPP reserve for the mid-term review – provided the funds were used for agriculture or rural areas. Both suggestions effectively reshuffle resources within the agricultural and cohesion envelope rather than expand it.

4.3 Structure and governance: how flexible is the budget – and who calls the shots?

If the overall budget cannot grow much, and demands keep multiplying, something else has to give. The Commission is betting on a strategy that tries to sidestep the most painful question – what exactly should be cut? – by aiming to make spending more efficient, flexible and faster to deploy, in the hope that the same euros might go further. To achieve this, the Commission has proposed a drastic redesign of both the MFF’s structure and the governance of funds.

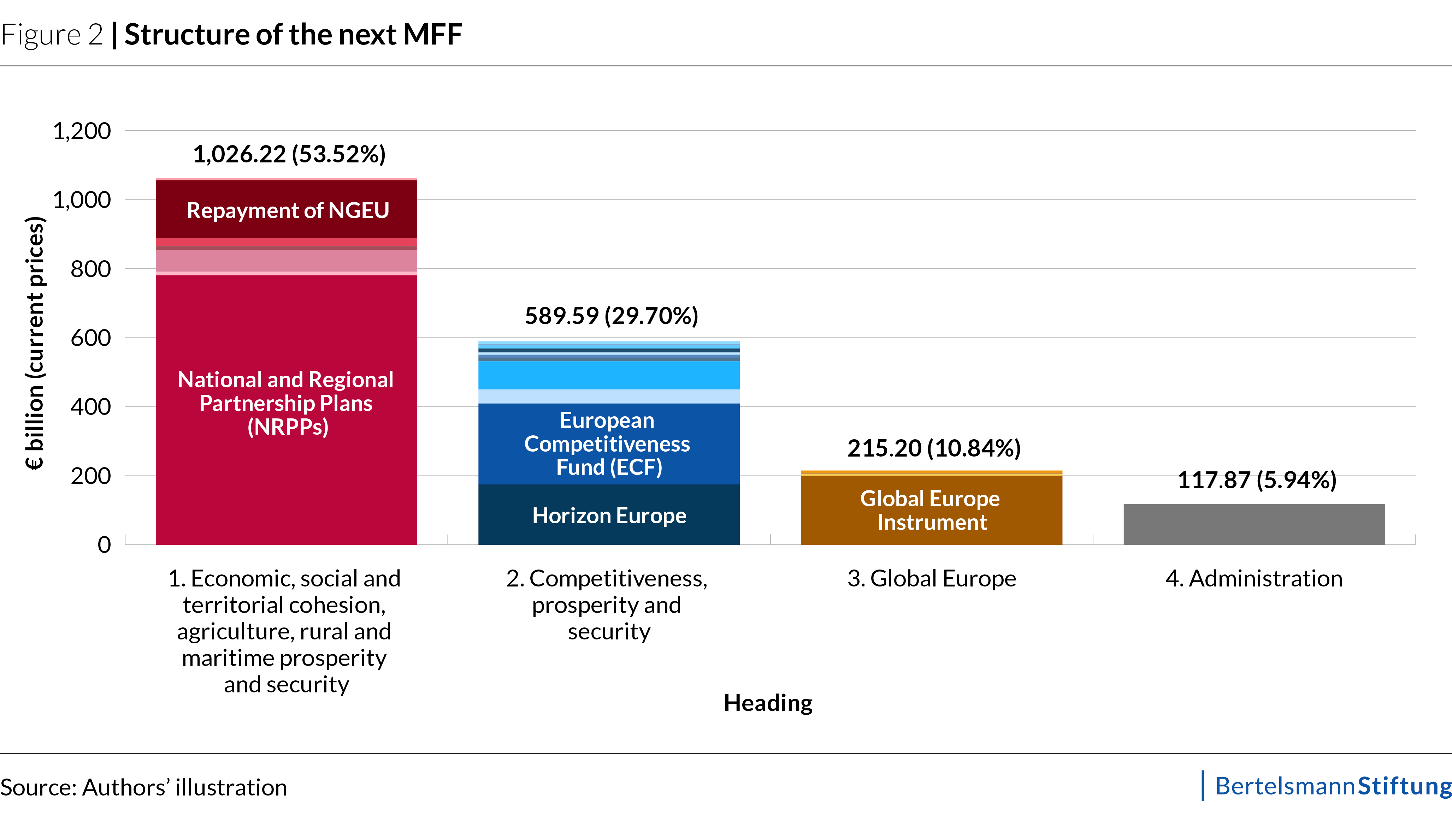

The current MFF resembles a carefully constructed labyrinth: numerous programmes, each with its own legal base, target groups and reporting logic, grouped into 15 clusters and seven headings. The new proposal moves in the opposite direction. It reduces the structure to four headings and roughly 20 larger funds (Figure 2). Consolidation is most visible – and most controversial – in two flagships: the National and Regional Partnership Plans (NRPPs) under Heading 1 and the European Competitiveness Fund (ECF) under Heading 2.

This redesign has already triggered strong resistance. So why go through all this trouble?

- Efficiency. Bringing previously separate instruments under a smaller number of larger programmes reduces fragmentation and enables funding at greater scale. Grouping related objectives within a single framework can make it easier to align investment strategies, create synergies and prevent different EU instruments from chasing similar goals under slightly different rules.

- Flexibility. Fewer and larger programmes give more room to reallocate funding in response to new developments without reopening MFF negotiations. That matters in a world where geopolitical shocks, industrial competition and security crises do not politely wait for the next seven-year cycle.

- Simplification: Harmonised eligibility rules, application procedures, and reporting requirements could lower transaction costs for both administrations and beneficiaries. At present, recipients can apply to several programmes for very similar activities under slightly different rules and without having a single point of entry. That creates clutter on all sides. If consolidation genuinely reduces that bureaucratic friction, it could widen access and free up resources for substantive investment rather than paperwork.

That is the promise. The risk, however, is equally structural. Flexibility inevitably creates distributional uncertainty. If funds can be shifted more easily within large programmes, some objectives and recipients will gain while others lose out. This is why debates about governance quickly follow debates about structure. Once programmes are merged and rules streamlined, the central question becomes: who gets to decide how the money is used? These tensions are most visible in the two flagship instruments.

One plan to plan them all: National and Regional Partnership Plans for shared-management programmes

With the proposed National and Regional Partnership Plans (NRPPs) under Heading 1, the Commission is attempting a fundamental redesign of shared-management funding. The idea is simple: one plan per Member State would set out how funds across shared-management instruments – from cohesion and agriculture to migration and internal security – are programmed and spent.

In doing so, the reform would make explicit what has long been implicit. Although the EU defines the overall framework for structural and agricultural funds, many key choices about priorities and implementation are made at national and regional level. By bundling allocations into one national envelope, the NRPP model would make clear to everyone who really calls the shots on detailed spending decisions. Unsurprisingly, this idea has triggered heavy resistance from regions, Parliament and the self-described “Friends of Cohesion”. Under the proposed system, regions would no longer have automatic access to specific pots of money. Instead, they would have to negotiate their share and justify its use within a national plan.

Predictably, consolidation has triggered calls for ringfencing. Parliament has already secured a 10% earmark for rural development. Farmers argue that the CAP should be kept outside the NRPP framework altogether. Social policy advocates and cohesion supporters demand dedicated shares for their priorities. The concerns that some priorities could lose out are understandable. But the more money is pre-allocated to specific goals, the more the NRPP model risks undermining exactly the efficiency, flexibility and simplicity it has been designed to deliver.

A second, equally contentious feature is the shift towards performance-based payments. Rather than reimbursing eligible expenditure project by project, payments would be linked to the achievement of country-specific milestones, drawing inspiration from the Recovery and Resilience Facility. The promise is greater alignment with EU priorities: milestones can turn shared-management funds into a more direct lever for reform. The risk lies in dependency. Regions fear that if a national government fails to meet agreed milestones, subnational beneficiaries will end up caught in the crossfire. Yet in many Member States, this interdependence is a feature not a bug. If regions have a stake in the national level meeting milestones, they have a stronger incentive to pressure national authorities to comply with EU commitments.

One fund to fund them all: a new Competitiveness Fund for direct management programmes

Under Heading 2, the proposed European Competitiveness Fund (ECF) would consolidate programmes linked to industrial policy and innovation under a single umbrella. At present, support for competitiveness and industrial policy is scattered across multiple programmes and administrative silos. By pooling instruments across areas such as defence, space, digital transition, health and climate, the ECF aims to build scale and reduce the fragmentation that currently hampers strategic, efficient EU investment.

Beyond consolidation, the ECF would alter how EU industrial priorities are set. Instead of locking them in at the beginning of the MFF cycle, the Commission would gain more discretion to steer funding through work programmes and to adjust priorities over the seven-year period.

That flexibility, however, is also the ECF’s central political fault line. If the Commission gains too much freedom to allocate and reallocate resources within a large fund, the ECF risks becoming less a strategic framework than a discretionary war chest used according to shifting political pressures. Flexibility matters in a volatile environment, but it needs credible guardrails. One option would be to anchor work programmes, in which the Commission sets the ECF’s priorities and instruments, more firmly in the annual budget procedure, combining stronger involvement of Member States and Parliament with clear deadlines for decision-making.

4.4 Human rights and rule-of-law conditionality: no money without values?

Human rights and rule-of-law conditionality is no longer peripheral. In the next MFF, it moves closer to the budget’s core architecture. The existing Conditionality Regulation will remain in force across the entire EU budget. It allows funds to be suspended where breaches of the rule of law threaten the Union’s financial interests.

What is new is the attempt to hardwire conditionality into shared-management spending through the NRPPs. The draft introduces two horizontal conditions: one on the rule of law and one on compliance with the Charter of Fundamental Rights. Member States would have to demonstrate in their plans how they meet these standards, with the Commission assessing compliance against the Rule of Law Report, the European Semester and country-specific recommendations.

If a condition is no longer fulfilled, the Commission could suspend part or all of the payments for the affected measures. Moreover, suspended funds would not remain frozen indefinitely. If the situation is not remedied within a year, the Member State would begin to lose the allocation, and the resources could be redirected elsewhere.

Horizontal conditionalities are bound to provoke resistance with Hungary as the most prominent case. From Budapest’s perspective, backing a budget from which it may not benefit as long as its rule-of-law dispute with the EU persists makes little sense. Orbán has already threatened to withhold support for the next MFF unless the EU releases funds currently suspended. The stage is set for confrontation.

4.5 Revenues: who pays?

Perhaps the biggest elephant in the Council is how to pay for all this. In practice, that means who contributes what.

By default, any increase in the EU budget is financed through higher national contributions based on GNI. As discussed earlier, additional own resources can alter how the financial burden is distributed, but they do not alter the overall amount that Member States need to pay. This is why everyone keeps searching for the holy grail – genuine own resources. Such resources tap into entirely new financial bases via the implementation of some EU policy – custom duties are the classic example – rather than simply being deduced off national budgets. Yet they always come with opportunity costs. If Member States were to raise similar revenue domestically, they could retain it. Most own resources proposed by the Commission, such as ETS revenues or the tobacco-based resource, do not meet the “genuineness” criterion because they draw on tax bases that are already being tapped. In practice, probably only CBAM and the handing fee for packages from third countries clearly do so.

There are nevertheless sound arguments for introducing new own resources. Some align with wider EU policy goals. Revenues linked to the Emissions Trading System (ETS) and the Carbon Border Adjustment Mechanism (CBAM), for example, aim to reduce CO2 emissions. The levy on non-recycled plastic packaging is designed to incentivise recycling. The most powerful argument, however, is political. In 2020, the Council and Parliament agreed that new resources should help finance the repayment of NGEU debt so that existing MFF programmes would not have to be cut.

The Commission has proposed a range of new own resources, including revenues based on ETS 1, CBAM, e-waste, tobacco and corporate turnover (“CORE”), as well as technical adjustments to existing own resources, such as a handling fee for low-value imports. Some proposals, including CBAM and the handling fee, enjoy relatively broad support. However, most of the others are far more controversial – especially those that would generate significant revenue such as the ETS-based resource, which would yield around €11 billion per year on average. By contrast, CBAM would yield less than €2 billion annually.

Progress on rebates has been equally limited. The Commission proposes abolishing the lump-sum corrections granted to some large net contributors. Unsurprisingly, countries which benefit from these corrections are not amused. And they have a point: rebates are a very blunt but also very transparent way of shifting part of the burden at the end negotiations rather than fiddling with the formulas of spending programmes or own resources. For that very reason, they will very likely be used again in this negotiation cycle.

Finally, the “D” question keeps returning: will EU debt once again be part of the solution – and when should it be repaid? The answer comes in three parts:

- First, yes – there will continue to be EU debt instruments. For decades, the EU has borrowed on capital markets to raise funds that it then lends on to third countries, for example through macro-financial assistance. In recent years, it has increasingly lent to its own Member States through programmes such as SURE, SAFE and NGEU. There is little reason to expect this to change. The built-in headroom (see section 2.2) exists precisely to make this borrowing possible.

- Second, what about rolling over part of the existing debt issued to finance NGEU spending (not loans), rather than beginning repayment immediately? Doing so could reduce the amount that needs to be set aside for debt service in the next MFF and temporarily free up resources for other priorities. But rolling over debt comes with a cost of its own. As every homeowner with a mortgage knows, if the principal is not repaid, interest continues to accrue.

- Third, could – and should – the EU issue new common debt to finance regular MFF spending? Three points matter here. To begin with, EU borrowing is not a free lunch. The EU typically pays more to borrow than its most creditworthy Member States, and following NGEU, a sizeable share of the budget will already be devoted to servicing existing debt. Any additional borrowing would therefore need to demonstrate clear added value to justify the extra cost. Second, the technical precedent now exists. NGEU showed how the EU can issue common debt to finance spending. Of course, that can be repeated if there is sufficient political will. Third, important legal constraints remain. There is no case law from the European Court of Justice yet on the full scope of permissible EU borrowing for common spending. What we do know comes from the German Constitutional Court. When greenlighting, NGEU, it made clear that authorisation to issue debt for spending must be included in the ORD and ratified by national parliaments. Moreover, borrowing is justified only under exceptional circumstances; ordinary budget spending must be financed through own resources.

As in previous MFF cycles, agreement on own resources and rebates is likely to emerge only in the final sprint of negotiations.

5. Conclusion

The next MFF will be negotiated under unusually tight political and fiscal constraints: rising expectations and shrinking national room for manoeuvre lead to a budget that is being asked to do more while remaining fundamentally limited in size. In this context, the negotiations will come down to a series of trade-offs that will lock in choices for seven years.

Three messages stand out.

- First, the pie will remain relatively small while new priorities are added on top. That means either agricultural and cohesion spending will need to shrink to create space for competitiveness, defence and other emerging priorities, or some of those new ambitions will have to be scaled back. “Show me your budget and I’ll tell you what you value.”

- Second, the Commission is trying to ease these trade-offs by making the budget more efficient and flexible. Two far–reaching reforms of the MFF’s structure and governance are on the table: the NRPPs with performance–based payments on the shared management side and the ECF on the direct–management side. Both could make spending more coherent, adaptable and strategically aligned with EU objectives. But they will not eliminate the trade-offs. And they will only deliver if they are not hollowed out by excessive ringfencing. At the same time, flexibility must be matched by clear and transparent governance – including credible involvement of both Member States and Parliament.

- Third, someone will have to pay – and that someone is always the Member States. There are good reasons to introduce new revenue sources, but they do not make the bill disappear. Whether the EU budget is financed through new own resources or higher national contributions, the primary effect is to redistribute costs among governments. Regardless, even for frugal Member States and net contributors, a higher contribution may be worthwhile – if it supports a genuinely modernised budget that puts real money behind the EU’s new priorities.

Download the Policy Brief (English)

Download the Policy Brief (German)

About the authors

Lucas Guttenberg heads our Europe programme as its Director. His own research focuses on the EU budget, EU economic and fiscal policy coordination, Germany’s role in the EU and the Franco-German relationship.

Anna Heckhausen works in the Europe programme at the Bertelsmann Stiftung, focusing on issues related to the EU budget.

Write a comment