Incubating Integration in the 28th Regime with Regulatory Pilots

How to test deeper harmonisation beyond company law

Few recent EU initiatives have attracted as much enthusiasm from founders and political leaders as the ‘28th regime’ – a single, opt-in European rulebook intended to simplify cross-border entrepreneurship. Its ambition is straightforward: to narrow Europe’s persistent innovation gap by reducing the legal fragmentation that hinders firms seeking to scale across member states.

That fragmentation carries significant costs. Companies face divergent national rules on insolvency, taxation, labour law and capital markets, among other areas. Yet resistance from member states to deeper integration in these domains is likely to confine the European Commission’s proposal for the regime to a comparatively narrow framework centred on company law. While politically feasible, such an approach would leave many of the regulatory barriers to scaling intact, limiting the regime’s economic impact.

The European Commission should use the current political momentum to develop a more ambitious single market instrument. Rather than postponing deeper integration to an uncertain future, it should pursue a dual strategy:

Establish a robust company law core: Develop a broadly accessible and coherent rulebook, accompanied by safeguards to prevent regulatory arbitrage and to secure political support.

Increase impact through regulatory pilots: Introduce targeted, time-limited pilots in areas where the economic gains from convergence are likely to be significant – including insolvency, labour mobility and accounting standards. These pilots would generate practical evidence to inform future integration in areas where progress has long stalled.

This approach would deliver immediate benefits for entrepreneurs while creating both the political space and the empirical foundation for deeper harmonisation. In doing so, it would strengthen not only the 28th regime itself but the functioning of the single market more broadly.

The EU faces an innovation gap vis-à-vis its global competitors. Although more startups are founded in Europe than in the United States, far fewer succeed in scaling. The EU accounts for only around 20% of the number of scale-ups found in the U.S. and hosts significantly fewer unicorns – 110 compared with 687 in the United States. Europe also trails in initial public offerings, representing just 11% of global initial public offerings (IPOs), compared with 38% in the United States and 18% in China (European Commission 2025).

Part of this scale-up deficit reflects fragmented capital markets and a shortage of risk capital. Venture Capital (VC) investment in the Union remains roughly 80–84% below U.S. levels across investment stages (European Commission 2025). Fragmentation keeps EU venture funds comparatively small and constrains cross-border investment flows. Investment patterns remain strongly home-biased: around 60% of startup investors are based in the company’s home country and only 20% in other member states. By contrast, the U.S. market is far more integrated, with roughly 30% of investment originating in the home state and 50% from other states (IMF 2025).

Scaling is also more costly because the single market remains incomplete. More than 62% of EU exporting firms report facing divergent national requirements when selling goods or services across borders (EIB 2025). The Commission notes that intra-EU trade has stagnated since 2022 and concludes that ‘integration has reached a plateau’ (European Commission 2026). Companies continue to navigate divergent national rulebooks across key policy areas, increasing complexity and compliance costs.

Efforts to reduce legal fragmentation have yielded only incremental progress. Although deeper integration in capital markets, taxation and labour mobility would lower costs and expand opportunities for firms, member states have been reluctant to agree on the necessary reforms. The most recent attempt at insolvency harmonisation illustrates the political constraint.

In this context, the Commission has announced plans for a 28th regime to support innovative firms in scaling across borders. Envisaged as an opt-in pan-European rulebook, the regime aims to reduce legal complexity for founders operating in multiple jurisdictions. The legislative proposal, expected in spring 2026, is likely to focus on company law for private limited liability companies, covering digital incorporation, minimum capital requirements, capital increases and employee stock ownership plans (ESOPs).

The 28th regime, however, is not a substitute for full harmonisation. Rather than replacing national legal frameworks with a single European rulebook, it would add a parallel layer. In effect, the Commission has opted for a political workaround, recognising that comprehensive harmonisation of company law remains unlikely in the near term.

If the regime is to deliver meaningful impact, it must be deployed strategically. A more harmonised company law framework for limited liability companies has clear merits, but it cannot alone address the broader regulatory fragmentation that constrains cross-border entrepreneurship. Given the political realities that have stalled deeper integration, the Commission should complement the company law core with targeted regulatory pilots in adjacent high-impact areas, such as insolvency. Carefully designed pilots would generate evidence, reduce political risk and help rebuild momentum for integration where tangible benefits can be demonstrated.

Entrepreneurs’ challenges in operating across borders

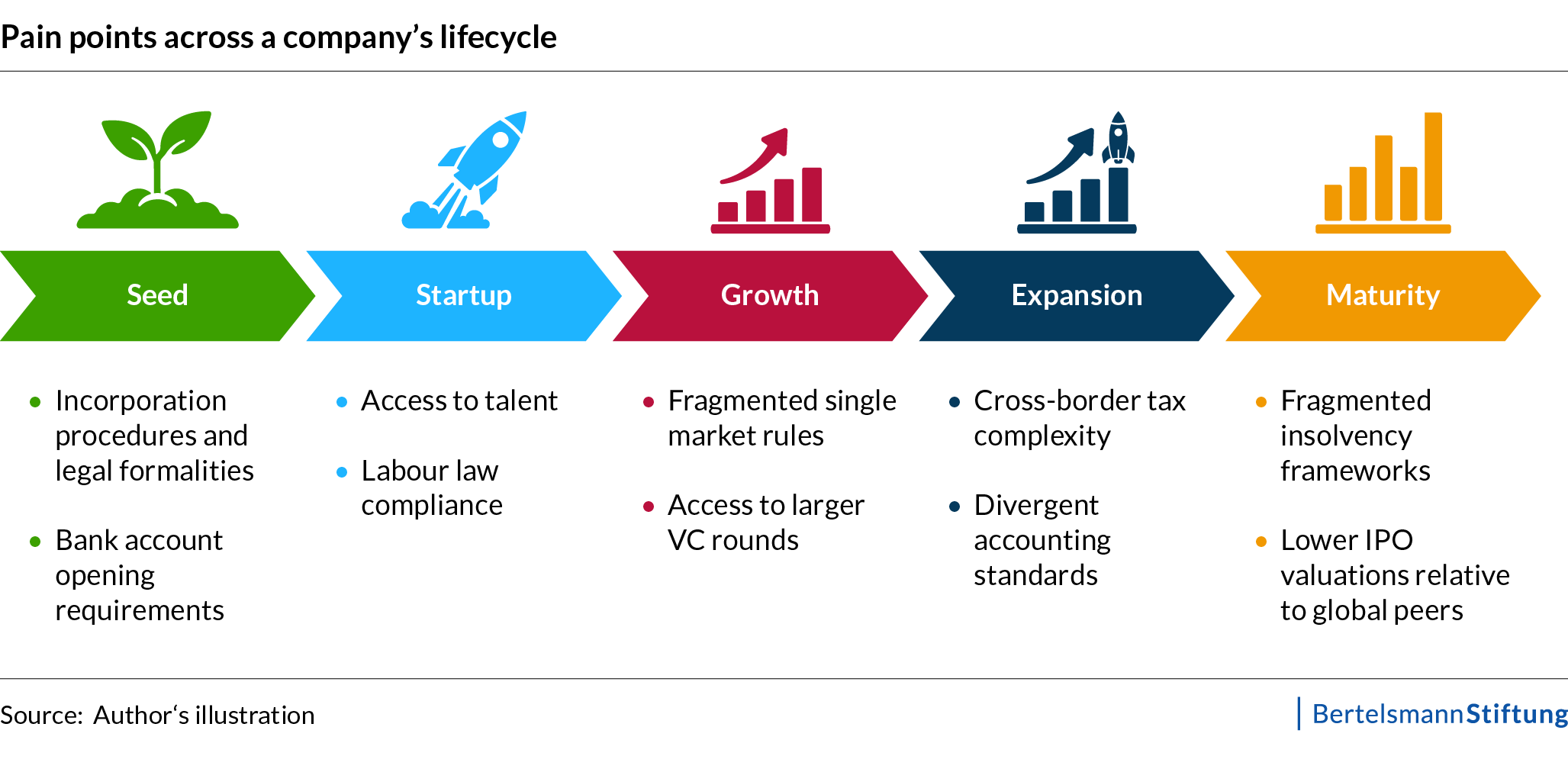

The Commission’s stated objective with the 28th regime is to reduce fragmentation and enable innovative firms to scale more rapidly. To assess what would be required to fulfil that ambition, it is useful to examine the constraints companies face across their life cycle (Figure 1).

From inception to exit, firms in Europe operate within a patchwork of 27 legal systems. Divergences in incorporation rules, corporate governance standards, taxation, labour law and accounting frameworks increase costs and administrative complexity – particularly once companies expand beyond their home market. These frictions hamper growth, productivity and investment (Draghi 2024).

Three examples illustrate how this fragmentation constrains firms in practice.

Access to talent: Startups are often unable to compete with established firms on salary alone and rely on employee stock options to attract skilled workers. Yet stock options are taxed differently across member states – sometimes as capital gains, sometimes as income – and at different stages, whether at grant or at exercise. Hiring from outside the EU presents additional hurdles, as visa procedures can be slow and restrictive. Furthermore, labour mobility across the Union continues to face structural barriers. Workers moving between countries encounter obstacles related to the portability of social security rights (IMF 2025).

Insolvency: Fragmentation also affects the end of the corporate life cycle. In the absence of a fully harmonised insolvency framework, national regimes differ on core elements such as creditor ranking (i.e. who is repaid when and in which order), the duration and efficiency of proceedings (Becker & Oehmke 2025). For cross-border investors, this creates uncertainty about getting their money back in the event of failure (Lindner & Mack 2024).

Administrative and legal divergence beyond labour and insolvency: Founders must navigate differing incorporation procedures, including practical bottlenecks such as opening bank accounts. Divergent tax systems and accounting standards add further layers of complexity for companies operating across borders and for their investors.

No single legislative measure can eliminate these barriers in one step. Meaningful progress would require coordinated action across several policy domains. Yet in the absence of political agreement on far-reaching reforms, the central question is not whether fragmentation can be removed entirely, but how the 28th regime can be designed to reduce it strategically despite existing constraints.

The current debate on the 28th regime: between ambition and political constraint

The prospect of a 28th regime has generated significant momentum. Following the Draghi and Letta reports, Commission President von der Leyen announced in early 2025 the creation of a single set of rules for companies operating across the Union. The initiative responds to long-standing demands from founders – including the EU-INC campaign – to reduce fragmentation and facilitate cross-border operations. Startups, business associations and political leaders have endorsed the project publicly, raising expectations of tangible improvements for scaling in Europe.

However, political constraints define the boundaries of what the regime can realistically deliver. Member states remain reluctant to relinquish national legal traditions. Unanimity requirements in sensitive areas such as taxation, combined with the EU’s limited competences in certain policy domains, have repeatedly stalled progress. Recent attempts at deeper harmonisation – including the latest insolvency directive and the stalled Business in Europe: Framework for Income Taxation (BEFIT) proposal on taxes – underscore the continuing limits to integration.

These constraints are evident in the debate over the legal form of the regime. A regulation would ensure uniform application across the Union but may require unanimity in the Council, raising the political threshold. A directive, by contrast, would be more feasible but would allow scope for national variation (see Schörner 2025).

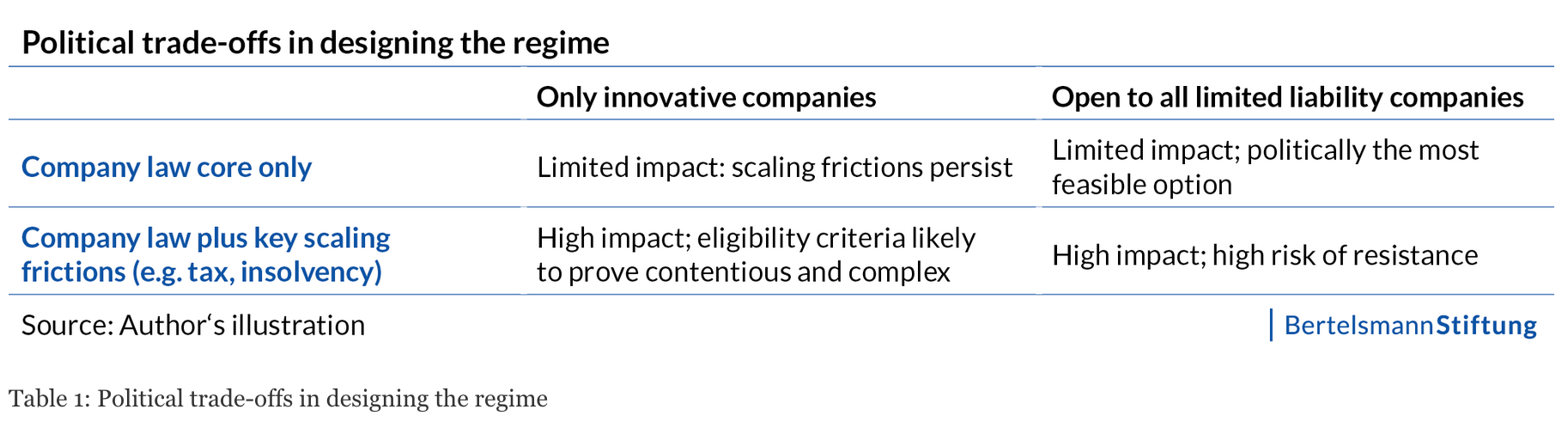

A parallel trade-off concerns the substance and the companies eligible to opt in. In principle, the 28th regime could encompass multiple policy areas and apply broadly. In practice, however, the same political constraints are likely to reassert themselves. As summarised in Table 1, the Commission faces a structural dilemma: a narrow regime focused primarily on company law is politically attainable but limits economic impact; a more comprehensive framework would promise greater gains but risks triggering resistance from member states and delaying adoption – particularly if, as the Commission has suggested, it is open to all limited liability companies rather than targeted at specific categories of firms.

Consequently, the debate has narrowed to company law as the most politically feasible starting point. This approach has clear advantages. As highlighted in the European Parliament’s own initiative report, a company law core could streamline cross-border incorporation, provide standardised templates for shareholder arrangements and improve the framework for employee stock option plans.

Opening the regime to all firms, however, raises legitimate concerns about forum shopping and regulatory arbitrage – the strategic exploitation of differences between national systems to minimise costs. Experience with the Societas Europaea (SE) has fuelled such apprehension. Trade unions, in particular, have warned that the regime could be used to circumvent national co-determination rules. Earlier efforts to introduce a European private company statute encountered similar resistance over worker protection. To avoid renewed backlash – and the potential derailment of the project – the Commission will need to embed credible safeguards that limit arbitrage while preserving the regime’s accessibility.

However, the proposed company law-centred approach would not address the broader legal fragmentation that constrains scaling. Corporate law does not operate in isolation; it is closely intertwined with taxation, labour regulation and insolvency frameworks. Reform limited to incorporation and governance would leave the broader fragmentation intact, requiring founders to continue navigating 27 parallel systems.

The debate is thus caught between necessary ambition and political feasibility. A broadly accessible regime confined to company law is the most likely to secure agreement but would deliver only incremental improvements. A comprehensive regime would offer greater benefits to startups and investors yet faces significant political headwinds. The Commission should use the 28th regime as a platform to test integration in high-impact areas through carefully designed pilots, creating a pathway to scale up reform where it proves both effective and politically sustainable.

Aiming higher: piloting harmonisation

If the 28th regime cannot deliver harmonisation across multiple policy fields in one step, it should be used strategically. The Commission should structure the 28th regime as a two-tier instrument that translates the current political momentum into a credible pathway towards deeper integration: a stable company law core combined with time-limited regulatory pilots in high-impact policy areas.

Regulatory pilots allow policymakers to test new rules before extending them more broadly. They introduce temporary and targeted frameworks to assess how specific regulatory approaches function in practice and whether they achieve their intended outcomes (OECD 2024). An EU precedent exists in the Distributed Ledger Technology (DLT) Pilot Regulation, which created a temporary framework permitting exemptions from certain financial market rules (European Commission 2023).

Embedding pilots as part of the 28th regime would offer a structured method for testing further harmonisation while containing political risk (Rohr 2025). Three design features are critical:

Time-limited application: Pilots would expire automatically after a defined period.

Restricted participation: Eligibility would be limited to a defined group of companies.

Evidence-based evaluation: Each pilot would be assessed against pre-defined performance indicators and benchmarks. Any extension or scaling would depend on whether those benchmarks are met.

Taken together, these features reduce political risk while producing the evidence needed to judge whether deeper integration is economically justified and politically viable.

How pilots could work: an insolvency example

Insolvency is a strong candidate for a regulatory pilot. Progress towards harmonising insolvency procedures in the EU has been slow, reflecting member states’ reluctance to relinquish control over deeply embedded national legal frameworks. Divergent regimes therefore persist. For cross-border investors, this fragmentation translates into legal uncertainty over recovery prospects in the event of failure. That uncertainty is priced into higher risk premia, which firms ultimately bear through increased financing costs.

An insolvency pilot could test a harmonised set of core rules for a defined cohort over a limited period. The objective would be to test the rules in practice and assess, on the basis of empirical evidence, whether they improve outcomes for entrepreneurs, investors and public authorities.

In substantive terms, the pilot could implement existing reform proposals in a controlled setting. To accommodate national sensitivities, experts have also advocated a ‘28th regime’ approach for insolvency law. While this idea has not yet gained sufficient political traction, detailed concepts for a harmonised insolvency regime already exist (e.g. Garcimartin and Paulus 2025). Rather than reinventing the wheel, the pilot could test core elements of these proposals, including restructuring procedures, creditor ranking and discharge rules.

Participation in the pilot would be capped. The scheme would apply to a limited number of companies – for example, 500 across the EU. It could focus, in particular, on innovative firms, which are often more exposed to restructuring and insolvency risks and frequently rely on venture capital funding that is partly constrained by fragmented insolvency regimes. Eligibility could therefore require firms to operate in at least two member states and to meet predefined innovation criteria. If applications exceed the cohort size, the Commission could select participants using a method that supports rigorous evaluation, including randomisation.

Once admitted, the insolvency pilot regime would apply to participating firms. Instead of following national insolvency rules, these firms would be subject to the harmonised pilot rules for the duration of the trial. For transparency, participation would be recorded publicly in the company register. Both existing and newly concluded contracts would fall under the pilot rules for as long as the firm remains in the pilot.

The pilot would be established through EU legislation incorporating a sunset clause. It would not alter national insolvency frameworks. Instead, it would operate alongside national law for a fixed period (e.g. 5 years) and would expire automatically unless political agreement is reached to extend or scale it.

Governance would be shared between the Commission and member states. Once the pilot is implemented, member states would designate national competent authorities and establish a specialised court chamber to handle proceedings under the pilot regime. Member states would also ensure non-discrimination towards participating firms. The Commission would support consistency in interpretation and oversee evaluation.

Rigorous evaluation would be integral to the pilot. From the outset, the Commission would establish an evaluation design, including appropriate counterfactuals. It would also define key performance indicators in advance, such as cross-border venture capital flows, recovery rates, time to discharge, restructuring versus liquidation rates and the cost of proceedings. Benchmarks for success (for example, proceedings that are 20% less costly than for comparable firms outside the pilot) would be specified upfront to enable an objective assessment.

The pilot would also need to address concerns affecting creditors and workers, including:

Safeguards: Although participation would be voluntary for companies, existing creditors and employees would also be affected by the applicable insolvency framework. The pilot should therefore include creditor and worker protection and anti-abuse provisions, as well as suspension or termination mechanisms in the event of significant distortions.

Run-off period: Insolvency proceedings may arise after the formal conclusion of the pilot. Investors require clarity, at the point of investment, regarding the insolvency rules that would apply in the event of failure. The pilot should therefore incorporate a predefined run-off period – for example, seven years – during which participating firms would remain subject to the pilot regime even after the trial has ended.

Finally, scaling of the pilots would not be automatic. On the basis of the evidence collected, the Commission would assess whether the predefined benchmarks have been met and determine whether to adapt, extend or scale the regime – for example, by proposing a permanent 28th insolvency framework or targeted further harmonisation of national insolvency rules. If political agreement among member states cannot be secured, the pilot would expire without follow-up. The general design principles are summarised in Figure 2.

This example illustrates how pilots could help advance integration in areas of high economic relevance. Rather than allowing debates on harmonisation to stall, pilots offer a time-bound and targeted mechanism for experimentation, reducing political risk while generating evidence to inform future decisions.

Where to start: high-impact pilot areas

Beyond insolvency, pilots should target policy areas that materially constrain cross-border firms and have proven politically difficult to harmonise. The emphasis should be on high-friction domains that can be tested within treaty limits.

Temporary labour mobility within the EU is another candidate for pilots. Posting workers for limited periods or enabling cross-border telework can trigger complex notification and compliance requirements (European Commission 2026). These administrative burdens reduce the attractiveness of providing services in other member states and narrow the range of arrangements firms can offer employees. A pilot could test coordinated simplification for a defined group of companies – for example, streamlined or waived declarations for short-term postings – to assess whether this leads to measurable increases in mobility.

Other areas may also lend themselves to experimentation. Accounting rules remain fragmented, particularly for small firms operating across multiple jurisdictions. A pilot could examine simplified and more harmonised accounting standards for cross-border companies. Similarly, selected elements of capital market regulation could be examined to evaluate whether targeted convergence improves access to cross-border financing.

Conclusion

The political momentum surrounding the 28th regime offers a unique opportunity to reduce fragmentation in the single market and ease structural constraints on founders. The current debate has generated significant enthusiasm, particularly within the startup community. Yet under current political conditions, a regime confined to company law is unlikely to deliver substantial improvements in cross-border scaling.

To deliver meaningful impact for founders, the Commission should deploy the 28th regime strategically. A robust company law core should serve as the foundation, complemented by targeted regulatory pilots in areas where harmonisation has repeatedly stalled.

Such an approach would allow the EU to test deeper integration under controlled conditions, generate credible evidence and contain political risk. If pilots demonstrate clear and measurable benefits – for example in insolvency – they could provide a sound basis for broader and more durable reform.

About the author

Claudia-Dominique Geiser is Senior Expert for EU economic policy in the Europe Program at the Bertelsmann Stiftung. Her focus is on EU single market policy.

Jake Benford, Brandon Bohrn, Lucas Resende Carvalho, Claudia-Dominique Geiser, Christian Hanelt, Anna Heckhausen, Etienne Höra, Cora Jungbluth, Miriam Kosmehl, Helena Quis, Torben Schütz, Peter Walkenhorst

Like what you're reading? The best way to keep up with our work is to subscribe to our newsletter.

Our Europe briefing with editorials by Daniela Schwarzer, Lucas Guttenberg and Malte Zabel lands in your mailbox twice a month, with information on our events, publications and the latest updates from our experts.

Write a comment